The Christmas and New Year break can often throw up significant volatility in international grain markets. The lack of liquidity with many participants on holidays means that moves can be exaggerated.

In international wheat

markets at least, we again saw some volatility in futures markets. Chicago Soft Red Wheat (SRW) jumped 5% higher

on boxing day and lost it all on the second of January and more on the third. All in all, SRW closed on Friday at 611¢/bushel,

basically where it was in the week before Christmas.

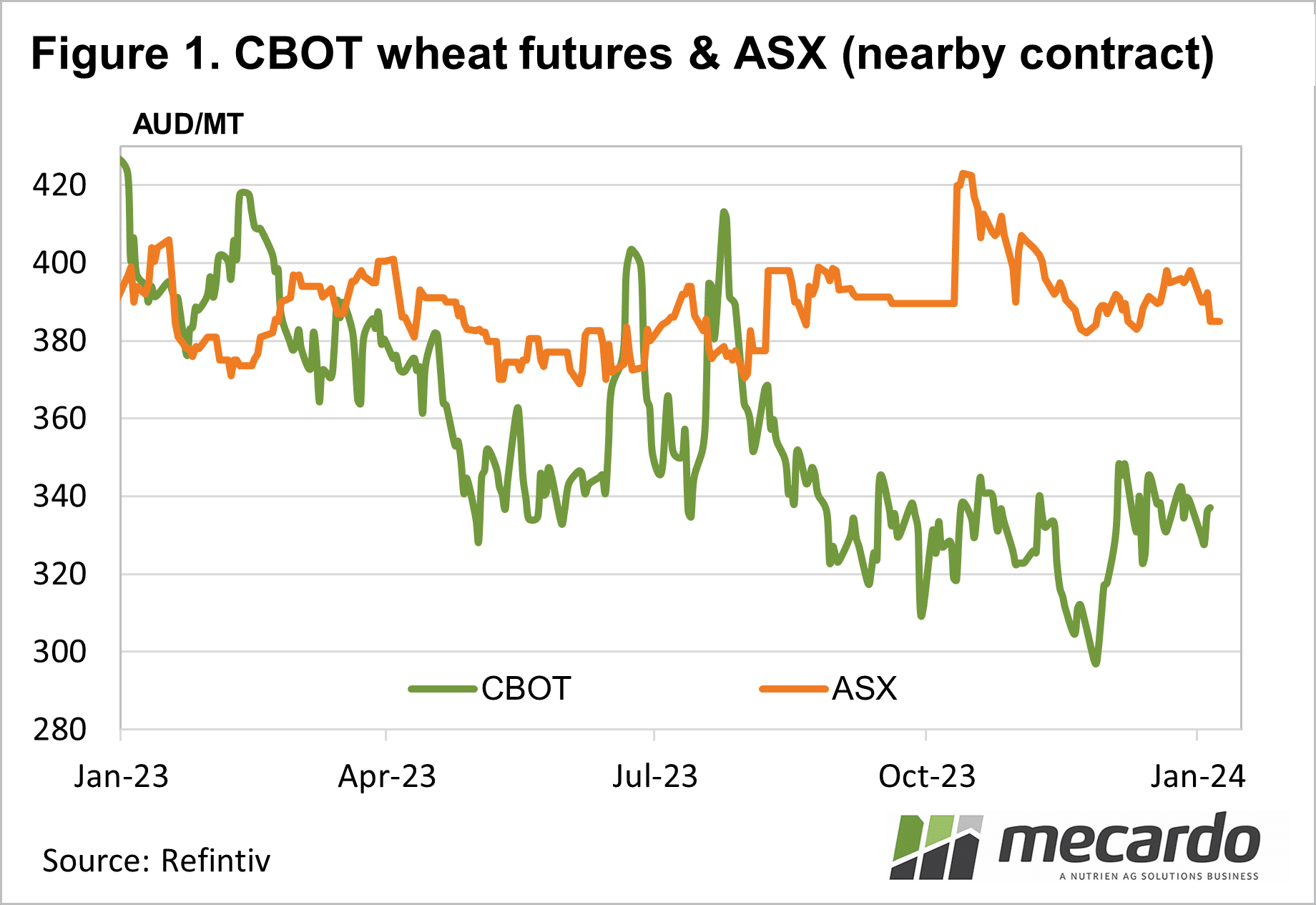

The Australian dollar

has remained relatively steady over the last few weeks. At 67US¢ the AUD is at the top of the recent

range and is keeping a lid on grain prices in our terms. Figure 1 shows that while SRW was bouncing

around, ASX wheat didn’t engage in the jump higher, but did partake in the New

Year fall.

ASX Wheat futures

finished last week at $385/t, its lowest point since the middle of December. It’s hard to remember now, but there was some

reasonable harvest weather over the last couple of weeks which put some

pressure on price. With the ASX premium

to SRW still close to $50, it’s not really surprising to see ASX easing

relative to SRW.

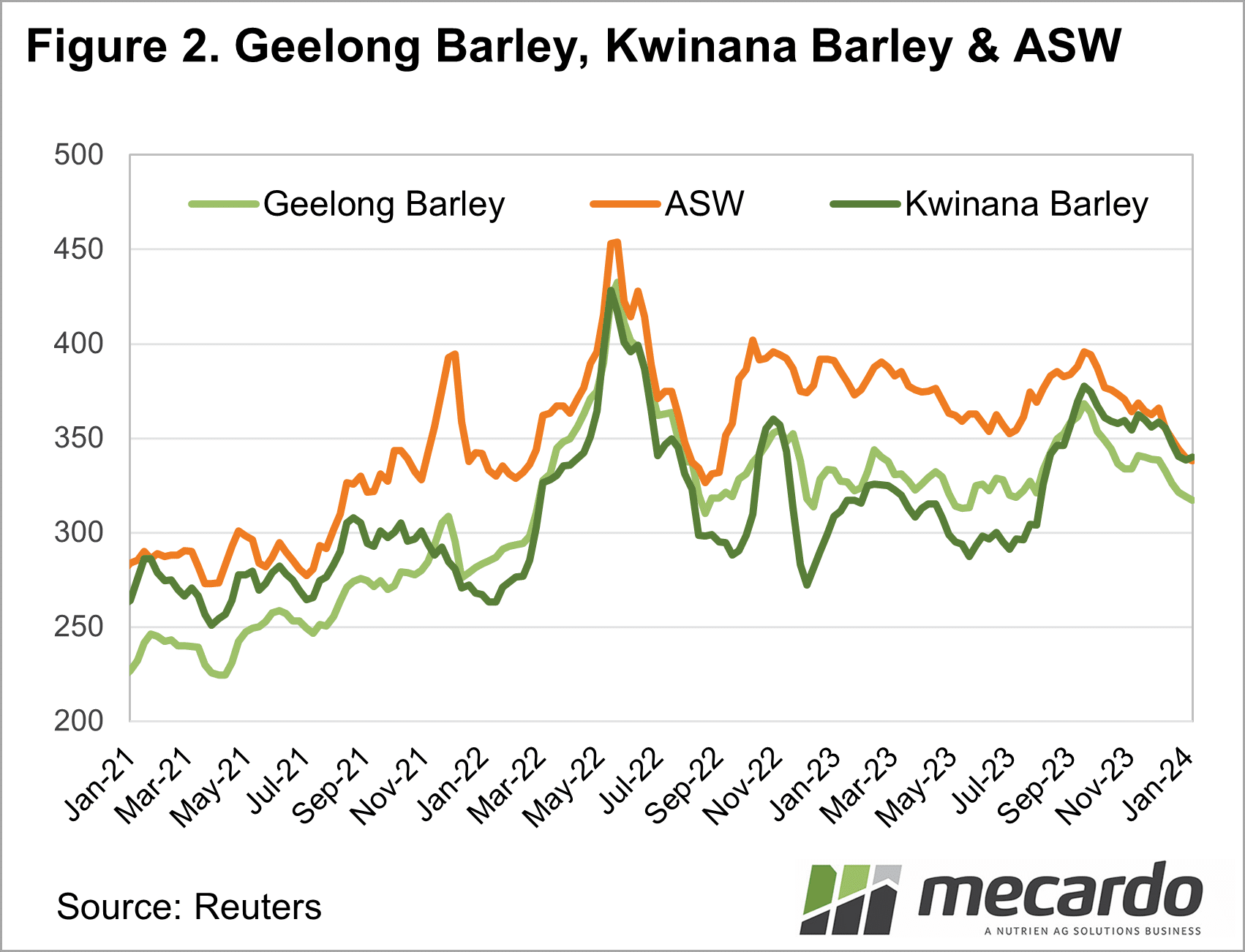

After the trade-induced

leap higher, barley prices have reverted to following local ASW markets, like they

used to (Figure 2). As feed substitutes,

ASW and barley have eased together over harvest, with supply concerns alleviated

with more downgraded wheat hitting the market due to wet weather.

At around $320/t in

Geelong, barley is almost back where it was before China reopened trade, while

the closer proximity to export markets in WA has seen prices hold on.

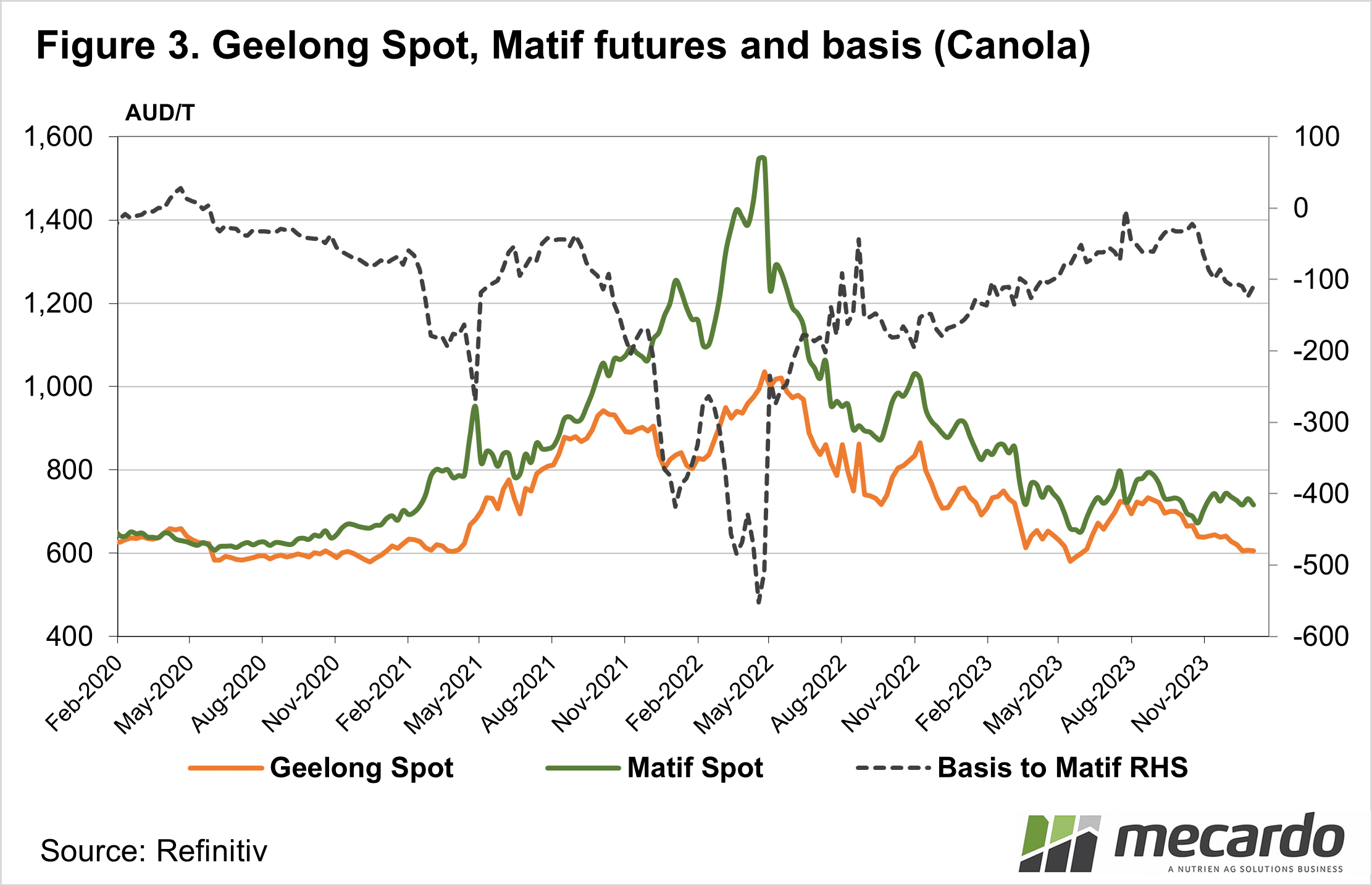

International canola

values have remained relatively steady over the break. Figure 3 shows Matif Rapeseed remaining in

the $710-720/t range for much of our harvest.

Local prices have been on a downward trend over harvest, with basis to

Matif remaining at a $100 discount.

There is some

potential for canola values to rally as selling pressure eases, but we are not

seeing any sign of that yet.

What does it mean?

The rally in SRW over the break was the only real action in international markets, while local prices eased. Early in the year is usually a time of some volatility as northern hemisphere crop prospects are uncertain.

Locally, basis can rally post-harvest, however, milling wheat is already at a good premium and the price of feed is around export levels.

Have any questions or comments?

Key Points

- There was some volatility in US wheat markets over the break, but local prices eased.

- Harvest pressure continued to keep a lid on physical price.

- Post-harvest rallies seem unlikely without improvement in international values.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, Mecardo