This article follows on from last week’s look at quality scheme volumes this season. Here we look to see if there is some appreciable price effect (preferably a premium) for RWS accredited wool sold at auction.

As the analysis last week showed (view here) only 1.3% of Merino fleece sold for the season to April was accredited RWS . To look for a price effect wool sales data has been filtered down in order to compare like for like, with the presence or absence of RWS accreditation the difference. The reality is that the methodology used here is a “first look” which requires stronger statistical analysis to give a greater level of confidence – this is a way of saying don’t take the price effects here as a given as there is considerable variation lot by lot in auction sales as exporters mix and match in an effort to both meet price targets and consignment requirements. In addition, many lots have multiple accreditations to quality schemes which possibly muddy the price effect even more.

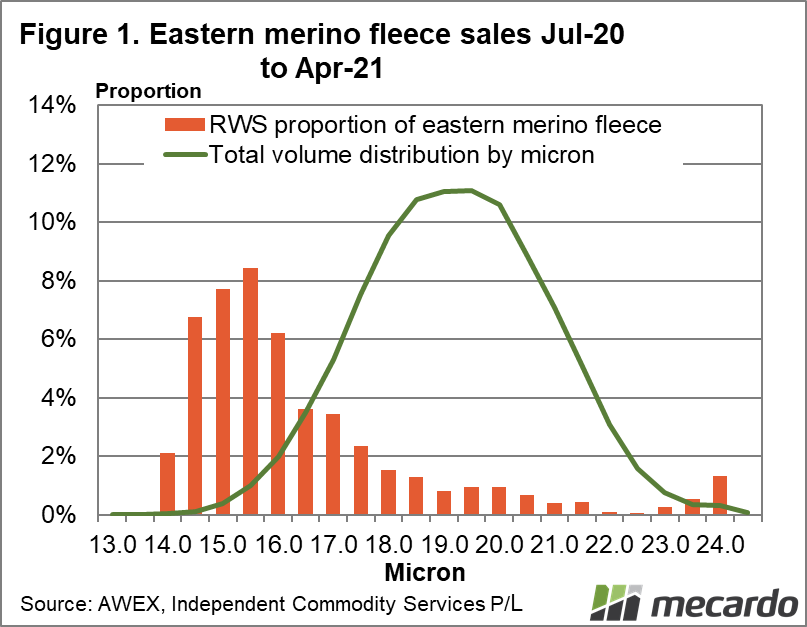

With the above caveat out of the way, Figure 1 shows the fibre diameter distribution of Merino fleece sold in the eastern centres (vegetable matter below 2%) from July 2020 to April 2021. This is provided to put some perspective on where the action is in auctions with regards to RWS wool. The bars in Figure 1 show the proportion of Merino fleece sold by half micron category which was accredited to RWS. For example for 16 micron, which made up about 2% of Merino fleece sales, some 6% was accredited to RWS. For the major Merino micron categories, around 1% is accredited to RWS.

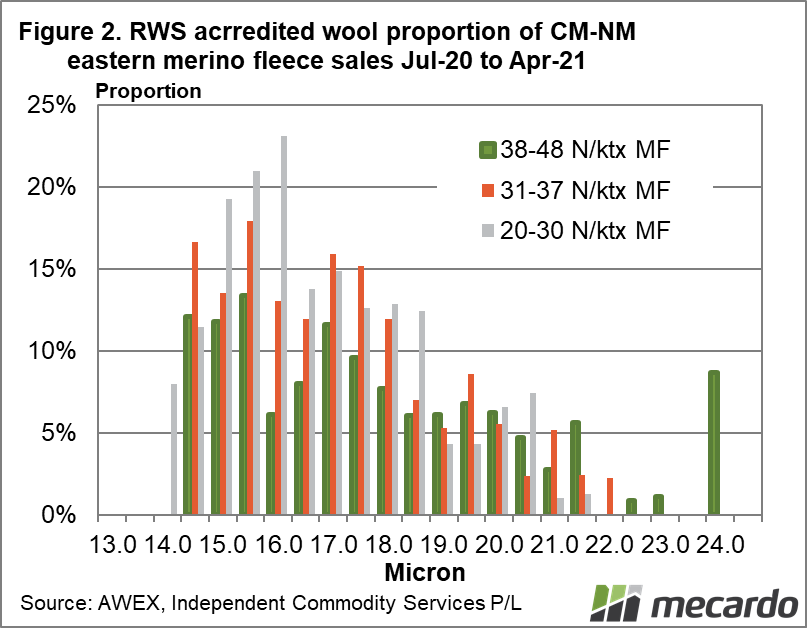

To look for a price effect the Merino fleece data was split into lots accredited to RWS and lots which were not accredited to RWS but were declared CM-NM. In February Mecardo published an article looking at the supply of CM-NM wool by micron (view here), which showed it, was heavily skewed to the finer Merino micron categories. Figure 2 shows the proportion of CM-NM Merino fleece wool by half micron category which was accredited to RWS for the season to April. For this step the data was to split by staple strength into three ranges. The proportion of RWS wool peaks around 16 micron, falling away to negligible levels for the broader Merinos.

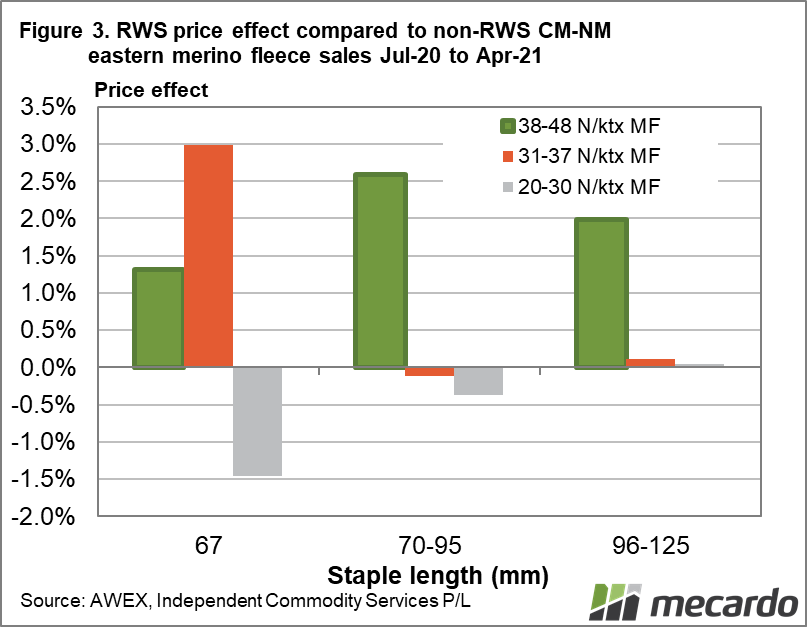

To tease out price effects the data further had to be broken up by staple length. Figure 3 provides the median price effect by staple strength by staple length for the season to April for RWS accredited Merino fleece, sold at auction. The price effect for lower staple strength categories is hit and miss, but for the 38-48 N/ktx staple strength range shows up as a consistent premium. There is some underlying logic that supports this in that direct contracts which use RWS as a quality standard tend to aim for higher staple strength, so this is where we would expect the buying interest at auction to be. In this “first look” approach it seems there is a premium for better performing Merino fleece accredited to RWS in the order of 2%.

What does it mean?

Around 10% of lower staple strength CM-NM Merino fleece was accredited to RWS in the season to April. For this wool, there appears to be no price benefit at auction, and it is unlikely direct contracts would have selected these lots. When the staple strength increases to high thirties and greater there does appear to be a premium in the order of 2%, which matches the demand for higher staple strength wool in direct contracts which have RWS as a stipulated requirement.

Have any questions or comments?

Key Points

- It seems there is a premium for RWS accredited Merino fleece, which has good specifications, in the order of 2%.

- For Merino fleece with lower staple strength, there appears to be no consistent premium, the price effect is too varied.

Data sources: ICS, AWEX, Mecardo