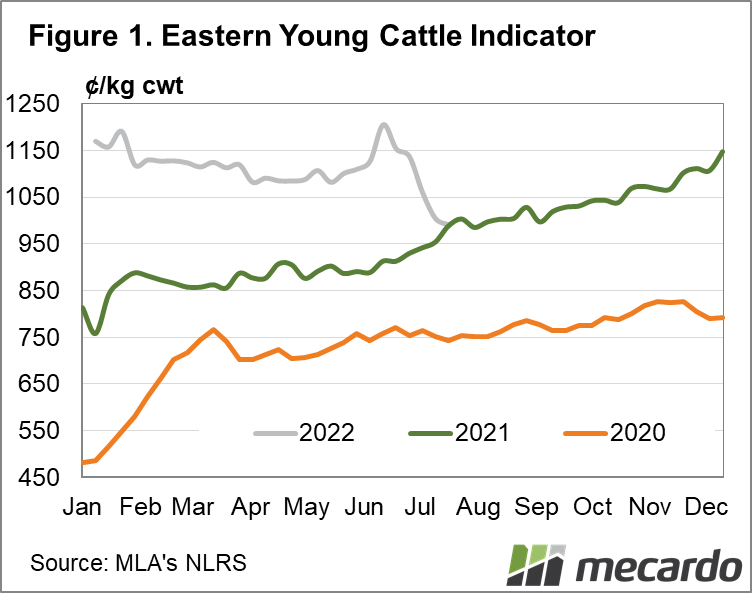

The dramatic fall in the Eastern Young Cattle Indicator (EYCI) in recent weeks has taken the market by surprise. July is normally a time of rising prices, but a few left field influences seem to have taken the sting out the market. So where is the support going to be found.

The slide in the EYCI show no sign of abating early this week. There was some sign of recovery last week, but Monday saw the indicator lose a further 13¢ to hit 992¢/kg cwt. Prices are by no means disastrous, they are still on a par with the same time last year.

Finding where prices are headed from here is the difficult part. There is a case to be made for a spring rally, similar to what we saw last year and in 2020 (figure 1). The argument goes that the current downturn has been caused by poorer quality cattle hitting the market, dragging prices lower. The spectre of Foot and Mouth Disease (FMD) is certainly not helping, and is no doubt impacting demand.

We can also see that paddock rates for feeders, and over the hooks rates for slaughter cattle haven’t eased as sharply as saleyards, which suggests quality cattle are still being sought after. As such spring restocker demand and better quality hitting the market should see saleyard indicators rise.

The other side of the argument is that we have seen the top, and the herd rebuild is finally seeing more young cattle available, which will continue through the spring. This will inevitably see further price declines.

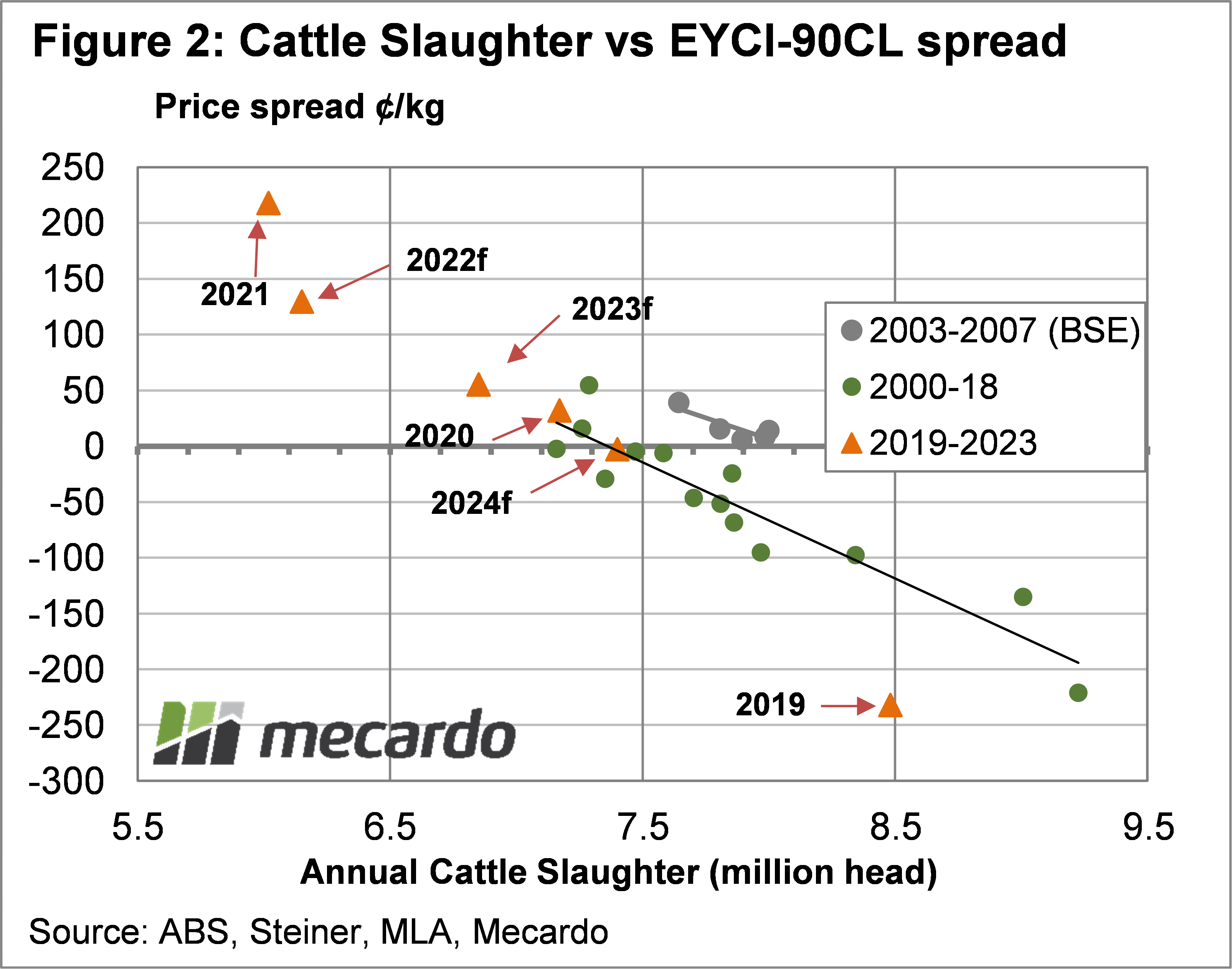

Long time readers will know that we use the 90CL Frozen Cow export price as a benchmark for international demand. As outlined last week, the EYCI premium to the 90CL has shrunk to 120¢. Historically the average premium is close to zero, but that doesn’t mean we’ve got another 120¢ of price falls to come.

Figure 2 shows how the annual cattle slaughter rate relates to the EYCI premium or discount to the 90CL. The trendline fits pretty well, with higher slaughter rates seeing a lower EYCI, and vice versa. Last year was a record premium for the EYCI, averaging 218¢, with slaughter just over 6 million.

Meat and Livestock Australia’s June cattle projections pegged slaughter for 2022 at 6.15 million head. Based on the trendline this puts the EYCI at a 129¢ premium to the 90CL. About where we are now.

What does it mean?

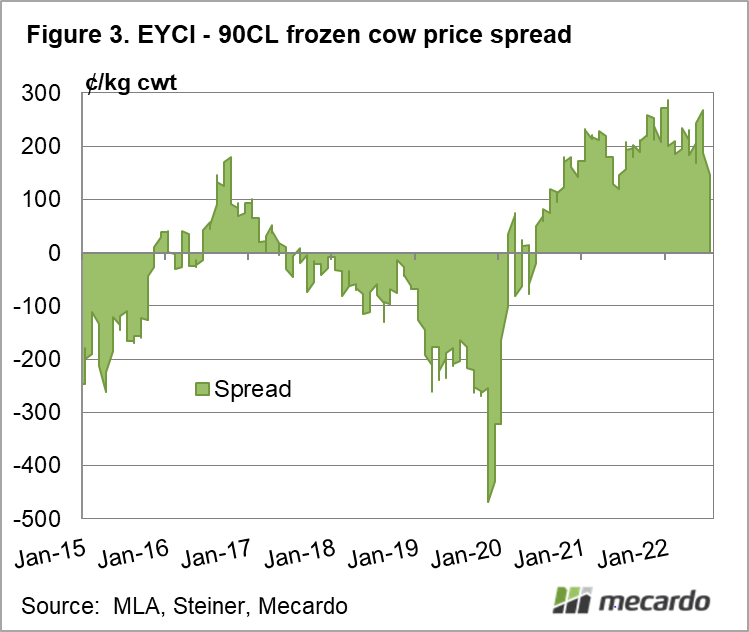

Rising spring supplies could push the EYCI lower relative to the 90CL, as the premium has averaged 212¢ for the year to date. To get back to an annual average of 129¢, it needs to be much lower for the remainder of the year.

However, there is a base in the market, and it’s not far away when we consider the EYCI has lost 130¢ in the last month. For prices to rally back to the 1100¢ level it’s likely we’ll need a good season, rising exports prices and easing FMD concerns.

Have any questions or comments?

Key Points

- The EYCI fall has taken the market by surprise, with a number of negative factors impacting saleyard values.

- Slaughter rates and export values points towards some further downside in prices.

- A price rise is likely to require renewed restocker demand and strong export prices.

Click on figure to expand

Click on figure to expand

Click on figure to expand

Data sources: MLA, Steiner, ABS, Mecardo