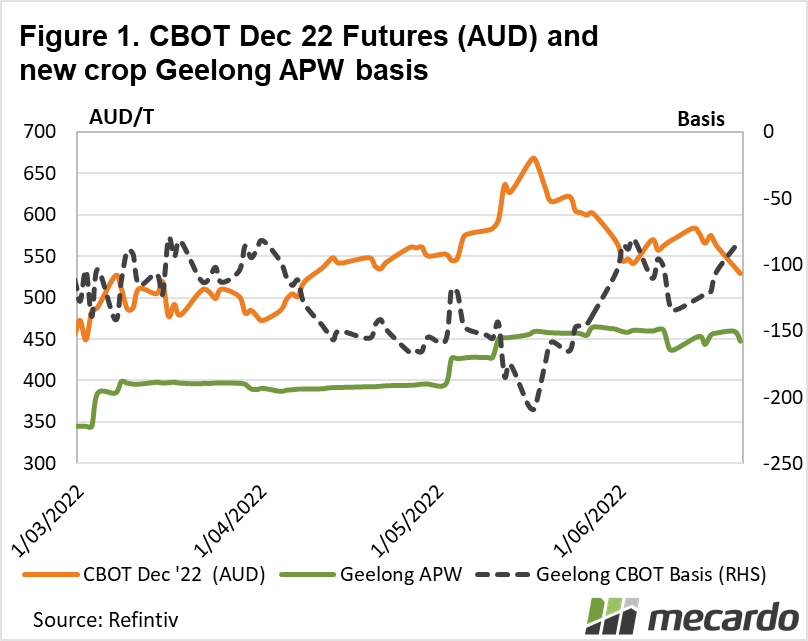

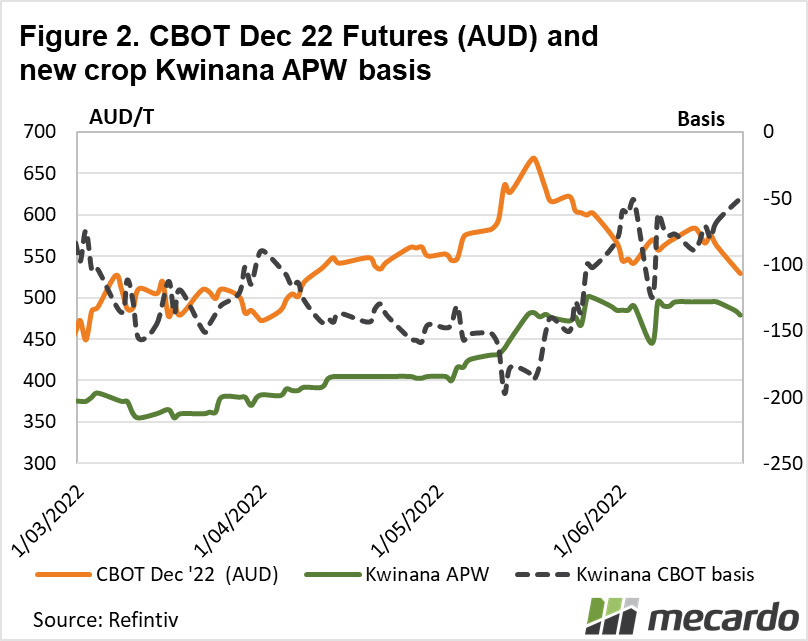

Where is the opportunity in SWAPS? Any keen market watcher will have noticed the discrepancy between AUD Futures (SWAPS) and the cash price. The spread (basis) between the two is trading at around -$100 for the new crop (Dec ’22) and around -$180 for the new, new crop Dec ’23 (referred to as the ‘red’ crop). Given basis usually firms as we get closer to our harvest, is there is an opportunity to hedge at a level that will give you a chance to outperform the cash price?

The problem with new season (Dec ’22) SWAP values is the underlying market drivers. As mentioned before, this season’s wheat market is hugely unpredictable and with it, volatility is through the roof. Tight stocks, production issues and the war in the Black Sea have all conspired to flip the market on its head. Prices for wheat are at or nearing all-time highs and a thin volume of market participants means that daily move ranges can be extremely wide.

The second issue comes with the assumption that we will see a basis improvement in the Aussie cash market. Australia is on the cusp of a third ‘record’ production year on the back of La Niña lingering through the first half of the year. Ports and up-country logistics are at capacity and despite a longer export tail than we might normally see, it is likely we will see carry out stocks build over consecutive years. This means that the trade will have access to old crop supplies as well as new crop when it becomes available during the peak shipping period between December – July. The need to ‘plump up’ the cash price (ie basis appreciation) will not be as great especially when futures values are so high.

In our mind, this spells trouble for SWAP holders in so much as the potential for a hedge loss combined with a steeply negative basis.

The opportunity perhaps lies in the red crop Dec ’23 season. Much of the premium built into the market price is due to the conflict in the Black Sea. We know that Turkey is trying to negotiate an ‘export corridor’ and we also know that the US is proposing short term storage facilities near the eastern border to help facilitate the storage and movement of grain into Europe. We also know that Russia is unlikely to weaken its own position at the expense of a hunger crisis.

As they say, necessity is the mother of invention and as time and the war drags on, the world will need Ukraine’s grain. It is likely that more and more Ukrainian grain will follow nontraditional pathways and make its way into Europe and other port zones not under blockade.

With this view, we potentially see a lessening of the supply chain disruptions. A return to greater supply channels and alternative trade routes, should allow for more transparency, less volatility and less confusion. Anything that allows Ukrainian grain into export channels will take time and this is the reason why we suspect that the red crop SWAP offers a better pricing opportunity.

What does it mean?

This remains an incredibly unpredictable market with many moving pieces. Tight stocks will mean there is an on-going price risk premium built into the market, but the removal, or at least easing of the Black Sea supply issues should result in a market that is considerably easier to trade.

Please note that this information should be considered general in nature and does not in any way taking into account your personal situation. Before entering into any derivative traded product, please read the appropriate PDS and speak to an authorised representative of an AFSL.

Have any questions or comments?

Key Points

- Large discrepancy between AUD futures and cash prices.

- Old crop supplies may limit basis improvement in the Aussie cash market at new crop harvest.

- Easing of Black Sea supply issues should result in a market easier to trade.

Click on figure to expand

Click on figure to expand

Data sources: Refinitiv, Mecardo