Mecardo has published quite a few articles on micron premiums and discounts in Merino prices, as it leads to substantial changes in relative prices and is related strongly to greasy wool production rather than change in demand along the supply chain which is much less transparent.

In late October, Mecardo showed how the micron price curves for short merino wool (including cardings) had picked up since mid-2019 in line with full length Merino combing wool. Underpinning changes to the micron premiums and discounts has been the broadening of the Merino clip (view article here).

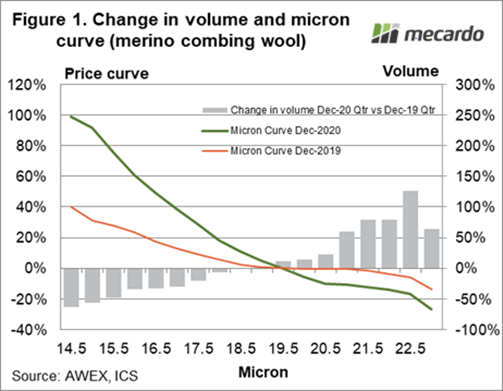

In Figure 1 the micron curve (where prices are indexed relative to the 19.5 micron price) for December 2020 and 2019 are shown (lines) with the change in Merino combing wool volumes sold at auction for the December 2020 and 2019 quarters shown by the bars. The price series used are combing fleece averages in half micron increments. The micron series runs from 14.5 to 23 micron. Changes in price and volume are sketchy beyond these micron categories as Merino volumes fall away quickly (on both the fine and broad ends of the distribution).

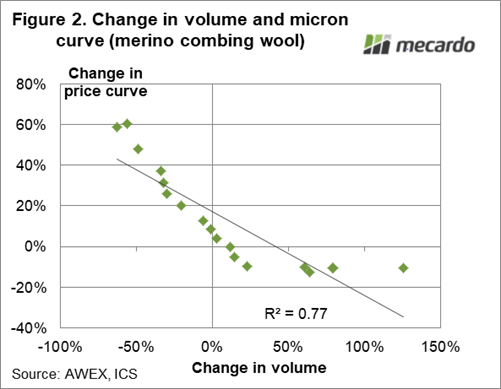

The schematic tells the story. Where supply has fallen, the micron price curve has risen and where supply has increased the micron price curve has fallen. Figure 2 compares the change in volume to the change in the micron premiums and discounts. By this measure the change in volume accounts for around three quarters of the change in micron premiums and discounts or price curve.

In December the 19.5 micron average combing fleece price was down 374 cents (clean) on the year earlier price (pre-pandemic). The increased fine micron premiums have offset this fall or more for 16.5 micron and finer wool, while the increased discounts for broad Merino wool have added to the fall in price.

The fibre diameter of the Australian Merino clip should continue to broaden until late this season, which means the pressure on these widening micron premiums and discounts will persist long into 2021. Given it is a La Niña year, Merinos in South America will be experiencing the opposite production trend. They will be getting finer, with increased premiums.

The main trends and cycles in the greasy wool market are driven by changes in demand, which emanate from a less than transparent supply chain. Relative prices between wool categories tend to be driven by supply (premiums and discounts for micron, vegetable fault, staple strength/mid-point break) so this analysis provides us with a rare chance to understand well what is driving a major price factor for some micron categories.

What does it mean?

Understanding the link between changes in Merino micron distributions and Merino micron premiums and discounts takes some of the mystery out of the wool market. It helps us understand some of the price volatility we have seen for fine and broad merino wool prices, which in itself is useful.

Have any questions or comments?

Key Points

- Change in supply accounts for around three quarters of the change in Merino micron and prices in the past 12 months.

- Given the expectation that the clip will continue to broaden through to late this season, the supply pressure will remain on Merino micron premiums and discounts well into 2021.

Click to expand

Click to expand

Data sources: AWEX, ICS, Mecardo