A common question regards what premiums for non-mulesed wool are present in the greasy wool market. In past articles, Mecardo has put the estimate of premiums to be in the range of 1% to 2%, with occasional direct contracts offering significantly higher premiums. This article takes a look at estimating average premiums for Merino combing fleece wool by micron for the past two years.

Earlier this year, Mecardo showed how the proportion of non-mulesed Merino wool sold was still quite low for the medium and broader micron categories, rising to quite high levels for the finer micron categories (see article). While volume plays a role in determining the ability to make valid price comparisons between non-mulesed and other wool, the complexity is compounded by quality systems (see March 21 article) and the role they play in delivering provenance through the supply chain, or at least that is the objective. In this article, we gloss over quality systems but we will have to come back in another article and consider them in conjunction with non-mulesed accreditation.

AWEX publishes weekly Premium and Discount Reports (view here) for each of the three wool selling centres (Sydney, Melbourne and Fremantle) which include an estimate for the price effect of non-mulesed, ceased mulesed and analgesic/anaesthetic accreditations on 18 to 25 micron Merino fleece. Your wool broker will have access to these reports.

Ultimately the people who know what premiums are operating, if any, in the market are exporters. Some exporters are on public record as supporting the supply of non-mulesed wool both by word and by chequebook (an old term which younger readers may have to google), but other exporters indicate a more varied level of demand for non-mulesed wool.

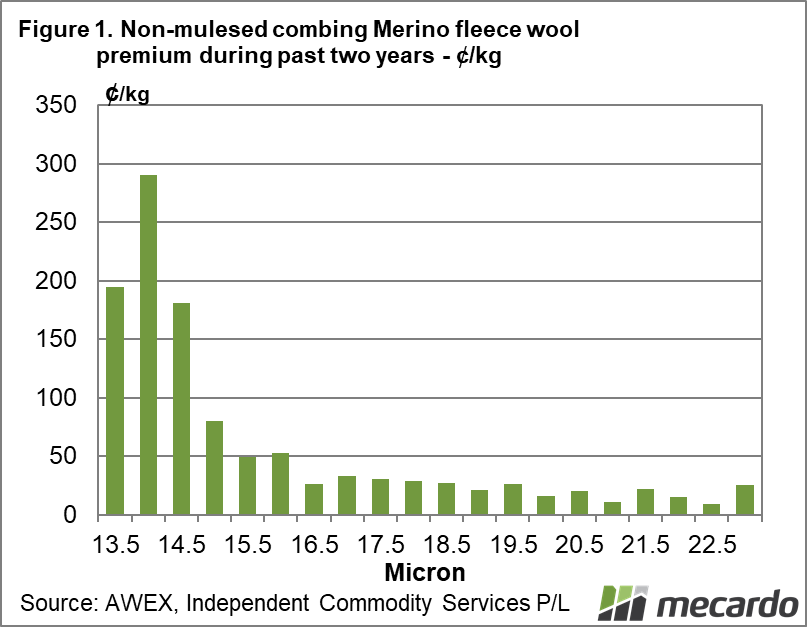

To arrive at Figure 1 monthly prices for ceased/non-mulesed and other combing Merino wool (sound, with vegetable fault below 2% and no subjective faults) were calculated in half micron increments for eastern Australia, averaged over the past 24 months and compared, to give an estimate of the underlying premium in the market. Week to week experience indicates such premiums ebb and flow. Figure 1 shows that premiums increase when the micron falls below 17-18 micron, rising to substantial levels for sub-15 micron. For the average Merino fibre diameter of 19 micron, the average premium has been in the order of 20 cents for the past two years. AWEX estimate the premium for19 micron to be currently 40 cents in the southern region (Melbourne).

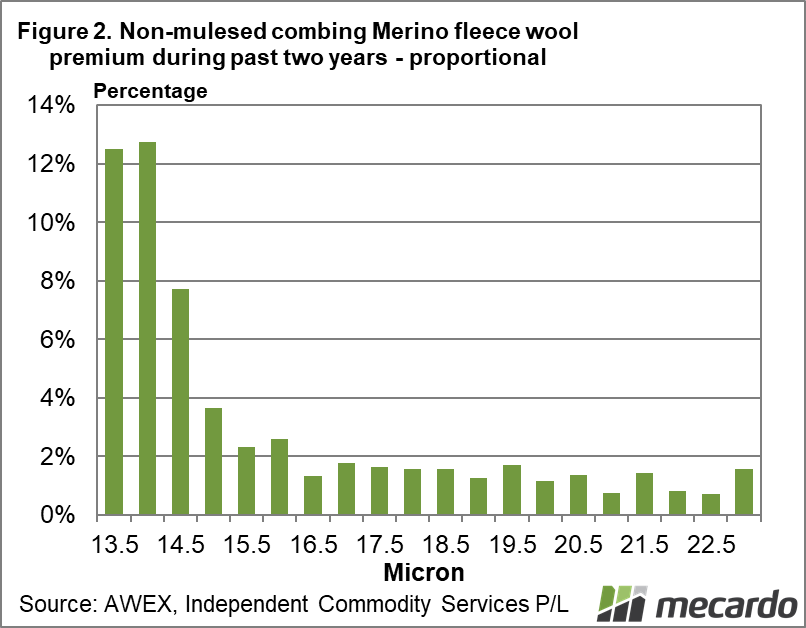

Figure 2 shows the same analysis but in percentage terms. For 19.5 through to 16.5 micron the premium ranges between 1.5% and 2%. It then starts to increase as the fibre diameter falls below 16 micron. The small price effect for medium and broad Merino (AWEX can’t see a price effect for broad Merino in the current market) means it can be easily swamped by other factors in the market such as within days price movements, or increases in vegetable fault discounts.

One explanation of why higher premiums are seen in the very finest micron categories is simply the limited nature of supply, making them a specialist fibre. During the past decade, the average annual sales value of 14 micron has been $2.9 million, compared to $260 million for 17 micron. An 8-10% premium for 17 micron would cost $21-$26 million per season.

What does it mean?

Once out of the rarified market of sub-16 micron, average premiums for non-mulesed wool settle down in the 1-2% range, falling away for the broader Merino micron categories. Non-mulesed accreditation can be a pre-requisite for direct contracts so the price performance at auction is only one measure of the benefit flowing to NM-CM wool.

Have any questions or comments?

Key Points

- For the bulk of the Merino combing fleece sold premiums of 1-2% for non-mulesed accreditation apply, albeit they are variable.

- For broader Merino wool the supply of non-mulesed wool remains low and premiums are minimal at the very best.

- Below 17 micron premiums for non-mulesed accreditation pick up as the fibre diameter falls.

Click to expand

Click to expand

Data sources: AWEX, ICS , Mecardo